Happy Wednesday. And yes, somehow it’s already New Year’s Eve.

If you’re reading this, odds are you fall into one of three camps tonight: you’re heading to a party (or pretending you will), you’re doing a late-night workout class because discipline is your personality now, or you’re parked on the couch watching AMC’s “Stranger Things” finale while pretending that counts as plans.

Normally, this space walks through five things to know before the opening bell. Today, that list would’ve included a surprisingly contentious set of Federal Reserve minutes and fresh details on SoftBank’s ever-expanding relationship with OpenAI.

But as 2025 comes to a close, it feels like the right moment to zoom out.

Because this year wasn’t defined by one earnings report, one CPI print, or one Fed meeting. It was shaped by a handful of forces that touched Wall Street, Main Street, and Silicon Valley all at once — sometimes pulling them together, sometimes tearing them apart.

Here are five themes investors should sit with as the calendar flips.

The stock market that refused to come back to earth

Against all odds, and frankly against a long list of reasonable objections, the stock market delivered again.

Major U.S. indexes notched fresh all-time highs in 2025, capping a third consecutive positive year. It didn’t feel easy while it was happening. In April, the S&P 500 briefly slipped into bear market territory after President Donald Trump unveiled a sweeping tariff plan that spooked investors and scrambled supply chains. Inflation never fully left the conversation. AI spending sparked both euphoria and anxiety.

And yet, the market climbed anyway.

Retail investors deserve a nod here. They aggressively bought the post-tariff dip and piled into momentum-heavy names like Nvidia and Palantir, often beating institutional caution to the punch. Wall Street, meanwhile, heads into 2026 expecting more gains — not less.

Even outside equities, risk assets had a moment. Precious metals soared. Crypto had flashes of life. Bonds? Not so much.

Here’s where things stand with one trading session left in the year:

| Asset | 2025 Performance |

|---|---|

| Dow Jones Industrial Average | +13.7% |

| S&P 500 | +17.3% |

| Nasdaq Composite | +21.3% |

| Russell 2000 | +12.1% |

| Gold | +66.1% |

| Silver | +166.5% |

| 10-Year Treasury | -13.1% |

| U.S. Dollar Index | -9.5% |

| WTI Crude Oil | -19.2% |

| Bitcoin | -5.8% |

The takeaway? Gravity took the year off. Valuations stretched. Skeptics stayed skeptical. The tape kept moving higher.

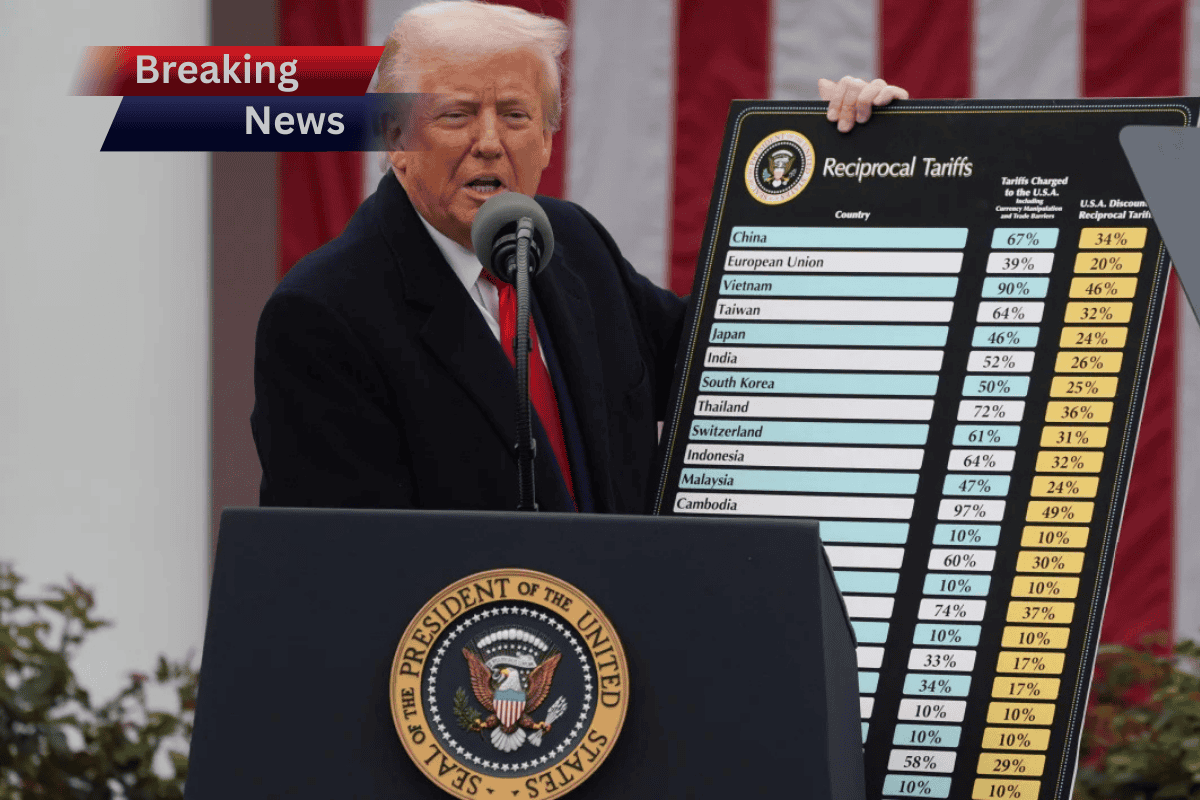

Trade-offs, tariffs, and uncertainty by design

Trump’s return to the White House didn’t just reshape politics. It reset the investment calendar.

Tariffs became the dominant macro variable almost overnight. Companies scrambled to rework supply chains ahead of broad duties on imports from major trading partners. Lobbying efforts exploded. Some firms scored carve-outs. Others didn’t.

Economists warned that tariffs could re-ignite inflation. Small businesses said — loudly — that they don’t have the margins to absorb higher costs the way multinationals do.

Now, the entire framework hangs in legal limbo.

The Supreme Court is weighing whether the new tariffs are constitutional. The administration has already signaled it has backup paths if the ruling goes against it. In other words: uncertainty isn’t going away. It’s just changing form.

For investors, trade policy in 2025 wasn’t about modeling precise outcomes. It was about understanding that volatility itself had become a feature.

The AI race that got very real, very fast

If 2024 was about AI promise, 2025 was about AI scale.

This was the year when artificial intelligence stopped being a software story and started looking like an industrial one. Nvidia, OpenAI, and their partners locked in multibillion-dollar commitments for chips, data centers, and power. Capital spending ballooned. Debt markets got involved. So did utilities.

Wall Street loved it — and feared it — at the same time.

AI-linked stocks powered a huge chunk of market gains. But the skeptics grew louder as the year went on. Is demand real or pulled forward? Are we overbuilding? What happens if growth slows before capacity comes online?

There’s no clean answer yet. What’s clear is that AI has rewired capital allocation decisions across tech, energy, and infrastructure. Even if the cycle cools, the spending already committed will shape markets for years.

As the Energy Information Administration has warned, data center power demand alone could materially alter regional grids this decade (https://www.eia.gov).

Fedfluence and the politics of interest rates

The Federal Reserve didn’t just set policy in 2025. It became the policy.

The Fed cut rates three times this year, bringing its benchmark into a 3.5%–3.75% range. For President Trump, that wasn’t enough. He openly pressured the central bank, floated firing Chair Jerome Powell, and went further by attempting to remove Fed Governor Lisa Cook — a move that remains tied up in court after the Supreme Court allowed her to stay on temporarily (https://www.supremecourt.gov).

The bigger story may be what comes next.

Powell’s term as chair ends in May 2026. Trump will get to nominate a successor. With policymakers already divided over how to balance a cooling labor market against sticky inflation, that appointment could tip the scales.

Markets are paying attention. So is the Fed.

A K-shaped economy that never quite healed

For consumers, 2025 felt uneven — and the data backs that up.

Higher-income households kept spending, especially on travel, premium services, and experiences. Airlines leaned hard into first-class expansions. Luxury held up. Meanwhile, lower-income consumers pulled back, gravitating toward discounts and value menus.

The “K-shaped economy” became shorthand for this divergence, and it explained a lot of otherwise confusing signals.

The job market added another layer. Hiring slowed. Firing stayed muted. For recent graduates, it was brutal. For policymakers, it was perplexing. Consumer sentiment hovered near historic lows even as markets rallied.

A prolonged government shutdown late in the year didn’t help confidence either.

Growth existed — but it didn’t feel shared.

What investors should carry into 2026

The unifying theme of 2025 wasn’t optimism or fear. It was imbalance.

Markets surged while consumers felt strained. AI boomed while questions multiplied. Policy uncertainty rose even as asset prices climbed.

That tension isn’t resolved as the year ends. It’s just paused for a holiday.

Whether 2026 brings a reckoning or another leg higher will depend on how these forces interact — not in isolation, but together.

FAQs

Why did stocks perform so well in 2025 despite uncertainty?

Strong earnings, AI-driven optimism, and aggressive dip-buying helped markets look past tariffs and inflation risks.

What role did tariffs play this year?

They increased volatility, reshaped supply chains, and added uncertainty, especially for small businesses.

Is the AI boom at risk of becoming a bubble?

Some investors worry about overcapacity, but demand remains strong. The risk is timing, not inevitability.

Why was the Federal Reserve so politically important in 2025?

Public pressure from the White House and upcoming leadership changes raised concerns about Fed independence.

What does a K-shaped economy mean for investors?

It suggests selective strength — companies serving high-income consumers often outperformed those reliant on price-sensitive demand.